How the Foreclosure Process Works in South Carolina (And What Your Options Are)

If you've fallen behind on your mortgage in South Carolina, you're not alone and you're not out of options. But you need to understand exactly what you're dealing with, because the foreclosure clock moves faster than most people expect.

South Carolina is a judicial foreclosure state, which means your lender has to take you to court before they can sell your home. That's both good news and bad news. Good, because you have legal protections and a defined timeline. Bad, because once the process starts, every missed deadline shrinks your options.

This guide breaks down each stage of the SC foreclosure process in plain language — no legal jargon — so you know exactly where you stand and what you can do about it.

Stage 1: Missed Payments and the 120-Day Window

Foreclosure doesn't start the day you miss a payment. Under federal law, your mortgage servicer can't file a foreclosure lawsuit until you're at least 120 days behind on payments. During this period, they're required to contact you to discuss options — things like loan modifications, forbearance, or repayment plans.

This is actually your most powerful window. You still have time to negotiate, and more importantly, you still have time to explore alternatives that keep the process out of court entirely.

Stage 2: The Breach Letter

While South Carolina law doesn't technically require a pre-foreclosure notice, almost every mortgage contract does. Your lender will send a breach letter — sometimes called a "notice of default" — telling you how much you owe, what you need to do to cure the default, and how long you have to do it (usually 30 days).

If you receive this letter, take it seriously. It means the lender is preparing to move forward. But it also means you still have time to act.

Stage 3: The Lawsuit Is Filed

Once the 120-day mark passes and you haven't resolved the default, the lender files a complaint in court. You'll be formally served with a summons and complaint — either in person or by publication if they can't locate you.

From the moment you're served, you have exactly 30 days to file a response. If you don't respond, the court will grant a default judgment, and the lender moves straight to scheduling a sale. Filing an answer buys you time and forces the lender to prove their case.

Stage 4: Court Proceedings

If you file an answer, the case moves through the court system. In South Carolina, foreclosure cases are heard by either a circuit court judge or a master-in-equity (a court-appointed officer who handles certain civil cases). The lender will typically file for summary judgment, arguing there's no genuine dispute — you owe the money, and you haven't paid it.

This stage can take anywhere from a few weeks to several months, depending on the court's docket and whether you raise valid defenses.

Stage 5: Judgment and Notice of Sale

Once the court issues a judgment in the lender's favor, the sale gets scheduled. By law, the sale must be advertised in a local newspaper once a week for three consecutive weeks and posted in three public places in the county, including the courthouse.

Foreclosure sales in South Carolina happen on the first Monday of each month (or Tuesday if Monday is a holiday), between 11:00 AM and 5:00 PM, on the courthouse steps.

Stage 6: The Foreclosure Sale and What Comes After

At the sale, the property goes to the highest bidder. Here's what most homeowners don't realize: if the home sells for less than what you owe, the lender can pursue a deficiency judgment against you for the difference. South Carolina has no anti-deficiency law protecting homeowners.

However, if the lender waives the deficiency, the sale closes after the bid. If they don't waive it, there's a 30-day upset bid period where anyone (including you) can submit a higher bid.

One more thing: South Carolina does not give you a right of redemption after the sale. Once the hammer falls and the upset period closes, the home is gone.

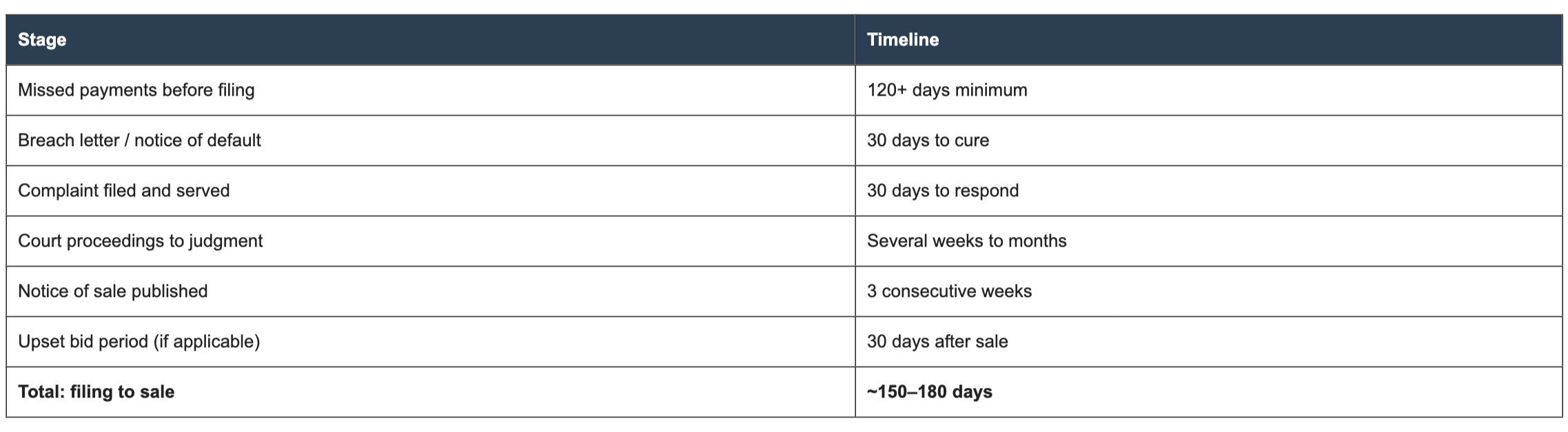

The Full Timeline at a Glance

What Are Your Options to Stop It?

Here's what most foreclosure guides won't tell you: the legal process is only one side of the story. The real question is what you can do about it — and the answer depends on where you are in the timeline.

Loan Modification or Forbearance

If you're in the early stages (pre-filing), your lender may agree to modify your loan terms or temporarily reduce payments. This works best if your hardship is temporary — a job loss, a medical issue — and you can demonstrate future ability to pay.

Sell the Home Before the Sale

You can sell your home at any point before the foreclosure sale is finalized. If you owe more than the home is worth, you may need lender approval for a short sale. If you have equity, a traditional sale or a direct cash sale can pay off the mortgage and stop the foreclosure entirely — often in a matter of days, not months.

File for Bankruptcy

Filing for Chapter 13 bankruptcy triggers an automatic stay, which immediately halts the foreclosure. This can buy significant time, but it comes with long-term financial consequences and requires court-supervised repayment.

Cash Sale to a Direct Buyer

This is the option most homeowners in foreclosure don't know about until it's almost too late. A direct cash buyer can close in as little as 7–14 days, pay off your existing mortgage, and stop the foreclosure before it hits your credit as a completed foreclosure. There are no repairs, no showings, no agent commissions, and no waiting for bank approvals.

For homeowners facing a hard deadline — especially those already served with a complaint — a cash sale is often the fastest and cleanest exit.

The Bottom Line

Foreclosure in South Carolina is a court-supervised process with real deadlines and real consequences. But at every stage, you have options — if you act before they expire. The biggest mistake we see homeowners make is waiting too long, assuming the problem will resolve itself or that they have more time than they actually do.

If you're behind on your mortgage and want to understand what a cash offer on your home would look like, we can walk you through the numbers in a straightforward, no-pressure conversation. We're Charleston Revival Homes — two College of Charleston graduates buying, renovating, and reinvesting in the neighborhoods we grew up in. We're BBB A+ accredited, and we don't wholesale your information to other buyers.

Learn more about how we help homeowners stop foreclosure →

Get a no-obligation cash offer in 24 hours →

Charleston Revival Homes buys houses in any condition across the Charleston metro area — including North Charleston, Mount Pleasant, Summerville, West Ashley, Goose Creek, James Island, Moncks Corner, Johns Island, Hanahan, and Ladson. If you're facing foreclosure, we can close on your timeline.